Australia has been grappling with recurring bushfires for over a century, significantly affecting the landscape and communities. Despite this, there has been an increase in residents moving into high-risk bushfire areas. This study aimed to develop a framework that could guide householder decision-making regarding self-evacuation during bushfires by identifying the incentives that encourage early evacuation. The study used a qualitative approach and 30 semi-structured interviews were conducted with residents in the southeast part of New South Wales; a region hardest hit during the 2019–20 summer bushfire season. Thirteen potential incentives that motivate self-evacuation were identified. The framework provides valuable insights into how incentives could influence residents’ decision-making during bushfires. In addition, it serves as a useful reference for policymakers, fire services and emergency management organisations when creating effective ways to encourage early self-evacuation and, ultimately, reduce injury and fatality.

Introduction

Australia experiences severe bushfires, yet there is a rise in the number of people relocating to bushland areas and an increase in the incidence of fatalities during catastrophic bushfires (Kremer 2018, Risk Frontiers 2020). Catastrophic bushfire seasons, such as Black Saturday in 2009 and the bushfires in the summer of 2019–20, have resulted in significant loss of life, claiming 173 and 35 lives, respectively (Edgeley & Paveglio 2019a, Risk Frontiers 2020). The recorded deaths due to bushfires have surpassed 825 for over 110 years of recorded bushfire seasons; 10 were catastrophic bushfires events and accounted for more than 60% of fatalities (Ambrey, Fleming & Manning 2017, Haynes et al. 2010, Risk Frontiers 2020). Along with these fatalities, Kohlbacher (2020) noted that the bushfires of 2019–20 also resulted in 429 smoke-related deaths, frequently resulting from delayed or non-evacuation. The physical and mental health cost of bushfires in Australia has soared dramatically. For example, the 2019–20 summer bushfires amounted to $1.95 billion, more than 9 times the median annual cost of bushfires for the previous 19 years ($211 million) (Ademi et al. 2023, Grattan Institute 2020, Kohlbacher 2020). These statistics emphasise the urgent necessity to scrutinise the factors influencing people’s decisions to self-evacuate from bushfire-prone areas including the increased bushfire severity due to climate change.

It is important to understand the factors contributing to people’s at-risk behaviour, particularly their decision to evacuate late during bushfire events, as evidenced by Strahan (2017). The alarming number of fatalities associated with bushfires has been linked to delayed or non-evacuation decisions, underscoring the need for effective ways to promote self-evacuation in at-risk communities (Edgeley & Paveglio 2019b, Whittaker et al. 2017). During the Black Saturday bushfires in 2009, despite 60% of householders indicating their intention to evacuate, only 2% followed through with their decision (Venn & Quiggin 2015), leading to devastating consequences. In Western Australia, Whittaker et al. (2017) reported that only 12 out of 300 residents indicated their intention to leave during bushfires. Tragically, during the Eyre Peninsula bushfires in South Australia, Anton and Lawrence (2016) found that 8 out of 9 householders died due to delayed evacuation. Their remains were discovered near their vehicles, demonstrating the severe consequences of failing to evacuate promptly. Given these findings, it is crucial to develop appropriate incentive programs that align with the factors influencing people’s decision-making.

Several studies highlight the effectiveness of incentives in encouraging self-evacuation, particularly in the context of voluntary evacuation (Adedokun et al. 2023, Perry 1979, Perry, Greene & Lindell 1980). However, bushfire policy is advisory and gives householders freedom to stay and defend or leave early (Whittaker, Taylor & Bearman 2020). In contrast, in the United States and Canada, evacuation is frequently compulsory, especially when properties are in the likely path of bushfires (McCaffrey, Rhodes & Stidham 2015). Notwithstanding the nature of policy in Australia, Adedokun et al. (2023) emphasise the need to investigate the role of incentives in influencing decision-making. This study aims to develop effective measures and interventions by acknowledging the severe consequences of late or non-evacuation and understanding the factors influencing decision-making. Specifically, it seeks to develop a framework that identifies and presents the influence of incentives on the cognitive processes involved in self-evacuation decisions. Using this model will allow relevant emergency management agencies to formulate targeted plans, align their interventions with the important incentives and enhance community resilience and safety during bushfires.

Materials and methods

An inductive research approach was used, which involved collecting qualitative data through semi-structured interviews with 30 participants. The purpose of the interview was to enable researchers to identify incentives that encourage early self-evacuation with a view to developing a framework that could guide decision-making. The method was chosen because it allows researchers to gain insights into the meanings behind the participants' views. Participants were recruited from southeast New South Wales, which was severely affected by bushfires between December 2019 and January 2020.

All participants provided written informed consent before the interviews. The recruitment process involved Sendaing flyers to participants through local council newsletters, community Facebook groups and notice boards. The participants were selected purposively from 3 local councils of Bega Valley Shire (population=33,253), Eurobodalla Shire (population=37,232) and Goulburn Mulwaree (population=29,609) councils as they had indicated an interest and willingness to participate in the study (Figure 1). The population figures presented were based on 2016 census data (IPWEA 2022, Owens & O’Kane 2020).

Participants were referred to in the study using alphanumeric codes rather than their names to ensure confidentiality. The interviews were conducted using a structured interview guide. The interviews were conducted face-to-face, online via zoom and by phone. Interviews lasted between 40 and 90 minutes. They were recorded, transcribed using Otter.AI and analysed using thematic content analysis via NVivo 12 Pro. This method involves identifying, analysing and reporting patterns or themes within the data.

Ethical approval for the study was given by the human research ethics committee of the University of Newcastle (Protocol Number H-2021-0284).

Figure 1: Map of New South Wales showing the study areas.

Results

Demographic information about interviewees

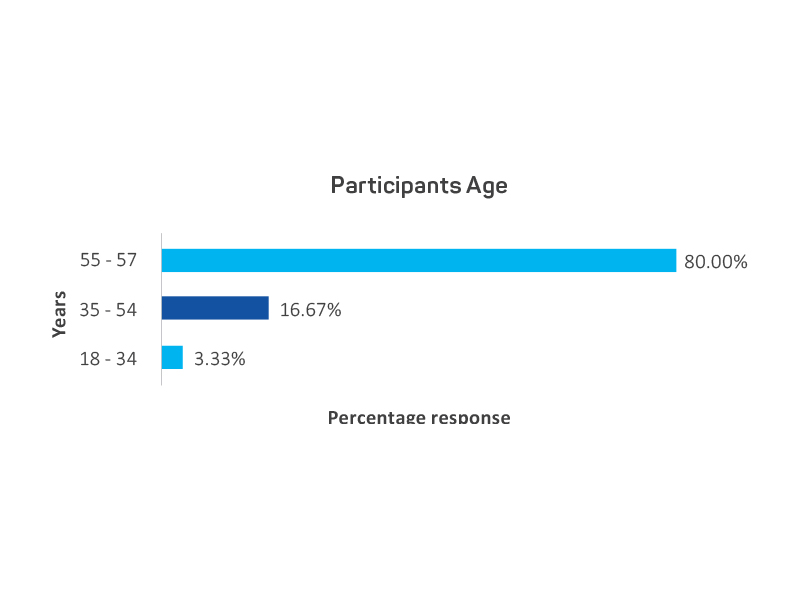

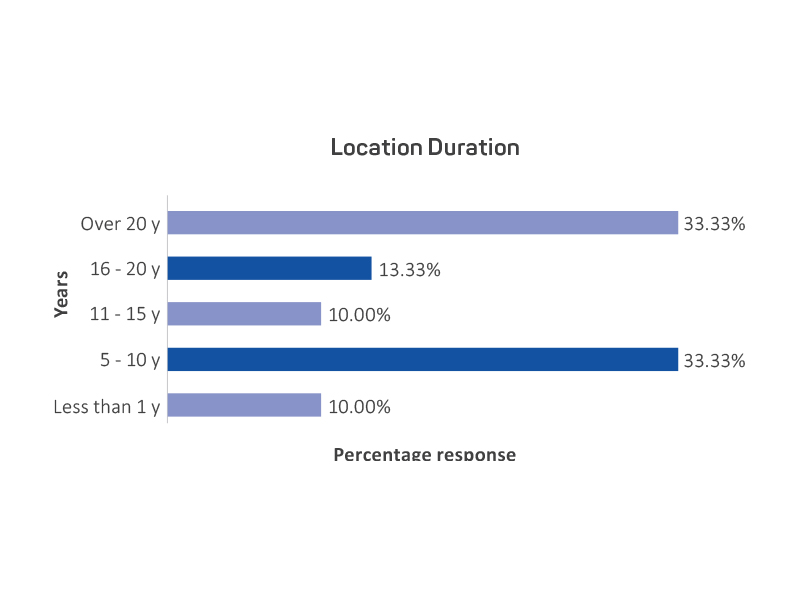

Figure 2 shows that most participants were 55–74 years old, making up 80% of the research participants. Additionally, 17% of participants were between 35–54 years old and the remaining 3% were between 18–34. The average age of participants was 60 years. They had been residing in their current location for an average of 13 years. Given their long-term residency, they were considered qualified to provide accounts of their bushfire experiences. For example, 33% had been living in at-risk bushfire areas for over 20 years, while 33% had been living in these areas for 5–10 years (Figure 3). A smaller proportion of participants, 13% and 10%, had been living in bushfire at-risk communities for 16–20 years and 5–10 years, respectively (Figure 3).

Figure 2: Percentage of participants by age.

Figure 3: Years participants lived in the location.

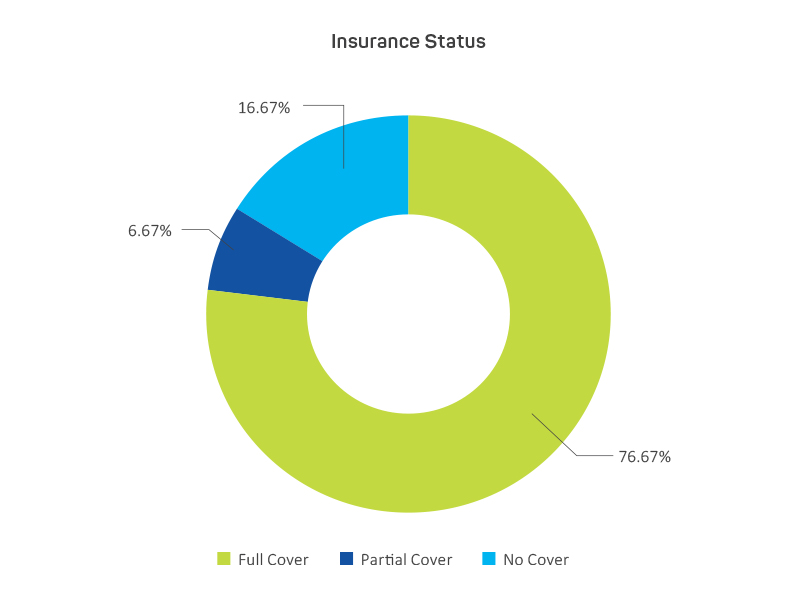

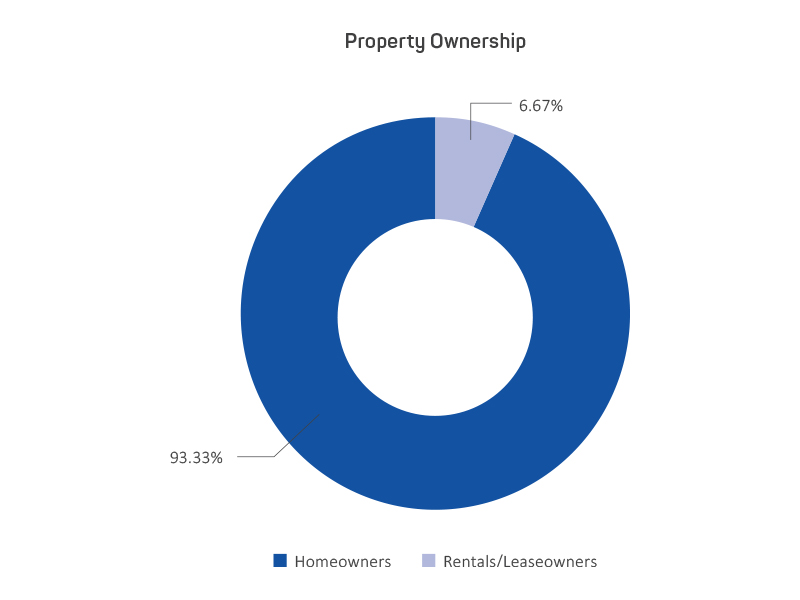

Figure 4 shows information about participants’ home and contents insurance status. The majority (77%) had full property insurance coverage. However, 17% did not have any insurance and 7% had partial coverage. While 93% of participants were home owners, the remaining 7% were renters or leaseholders (Figure 5). The 7% proportion might explain why some participants were not insured, as leaseholders cannot insure property they do not own.

Figure 4: Percentage of participants with insurance.

Figure 5: Percentage of participants owning or renting their home.

Figure 6 shows that 80% of the participants had pets or animals, while 20% did not. On average, the interviewees lived within 59 metres of bushland (Figure 7).

Figure 6: Percentage of participants owning a pet.

Figure 7: Distance from bushland of participants.

Incentives that could encourage self-evacuation

Figure 8 shows an overview of the incentives that could encourage self-evacuation from bushfire-prone areas as selected by participants. The most common incentives identified by participants were information and communication (60%), adequacy of resourcing the Rural Fire Service (37%), for example firefighters, fire trucks and training and emergency accommodation (33%). Other incentives included bushfire education programs (27%), vegetation management (17%), financial assistance (17%), access roads (13%), security and protection of property (10%), affordable insurance coverage (10%), alternative power supplies (10%), property preparation assistance (7%), return access to properties (3%) and improved development approval procedures (3%).

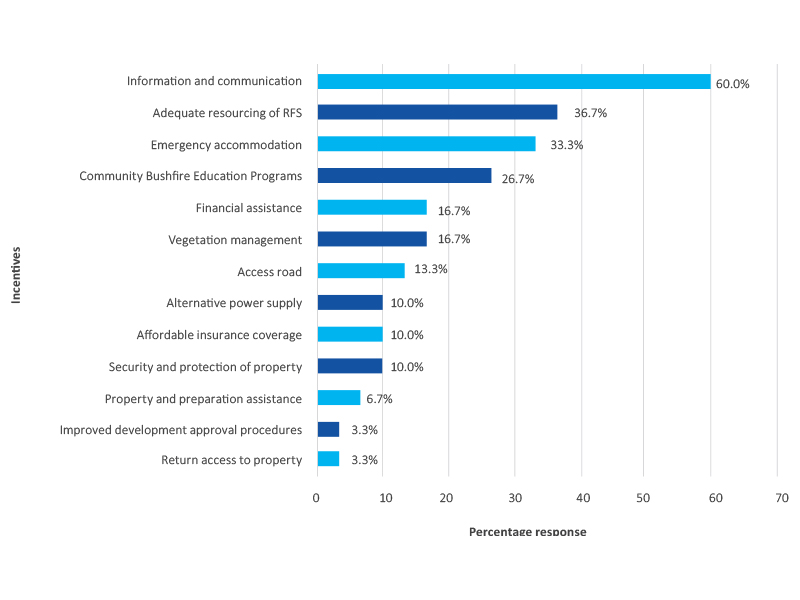

Overall, 41% of male and 59% of female participants mentioned these incentives and shows that more women were willing to evacuate than their male counterparts. Participants’ ages ranged between 18 and 74 years and suggests that incentives could encourage evacuation across all age groups. Most of the participants had pets, which could make evacuation challenging, while 20% did not have pets.

These data suggest that a combination of incentives could encourage self-evacuation from bushfire-prone areas, with information and communication being the essential incentives that participants identified. Adequacy of resourcing the Rural Fire Service, emergency accommodation and bushfire education programs were identified as essential incentives. These findings could help develop policies and plans to encourage self-evacuation from bushfire-prone areas, particularly among households with pets.

Development of a self-evacuation decision framework

Figure 8 shows the incentives could inform self-evacuation decisions in response to bushfire threats. The aim is to make the framework simple and easy to understand for use by fire service agencies in charge of evacuating people as well as by policymakers and academics. The shared experiences of participants about the incentives that could encourage self-evacuation provides insights that can be used to identify how these incentives could influence their decision-making processes.

Figure 8: Potential incentives that could encouraging self-evacuation.

Figure 9 shows the framework and represents the conceptualisation drawn from the analyses of the interview data and the outcomes of the analyses in this study. The incentives were linked to threat and coping appraisal components of the framework. The threat appraisal component comprises perceived severity, vulnerability, concern, likelihood and reward (maladaptive). The coping appraisal component includes perceived self-efficacy, response efficacy and perceived cost (adaptive response) of evacuation.

Figure 9: The developed self-evacuation decision framework. Note: Coping appraisal refers to the attitude towards self-evacuation in response to bushfire.

Four incentives with the potential to influence both threat and coping appraisal components were identified. These are information and communication, adequacy of resourcing the Rural Fire Service, bushfire education programs and vegetation management (Figure 9). Nine additional incentives that could affect coping appraisal were identified, including emergency accommodation, financial assistance, access roads, security and protection of property, affordable insurance coverage, alternative power supplies, property preparation assistance, return access to properties and improved development approval procedures.

The self-evacuation decision framework

Threat appraisal construct

Table 1 shows the conditions under which threat appraisal can be high considering levels of perceived concern, likelihood, severity, vulnerability and low levels of maladaptive rewards. If a householder perceives high levels of concern, likelihood, severity and vulnerability associated with a bushfire and low levels of maladaptive perceived rewards, then their threat appraisal is likely to be high (Booth, Lucas & French 2022; Oswald 2021).

Table 1: Factors informing the threat appraisal construct.

| Perceived Factor | High Level | Threat Appraisal Level |

| Perceived Bushfire Concern | Yes | High |

| Perceived Bushfire Likelihood | Yes | |

| Perceived Bushfire Severity | Yes | |

| Perceived Bushfire Vulnerability | Yes | |

| Perceived Rewards (Maladaptive) | No |

This concern can arise from experiencing or witnessing previous devastating bushfires or living in an area that has recently experienced high temperatures and dry conditions, which increases the likelihood of bushfires (Molan & Weber 2021, Strahan & Gilbert 2021a, Strahan & Gilbert 2021b). The severity of the potential impact on their safety, wellbeing, property and perceived vulnerability can also increase their threat appraisal (Bowman et al. 2020, Lake & Christianson 2020).

Coping appraisal construct

Table 2 shows the conditions under which coping appraisal can be high, considering householders perceived self-efficacy, perceived response efficacy and perceived cost. Suppose a householder perceives high self-efficacy and response efficacy and low costs (adaptive response) associated with a bushfire. In that case, their coping appraisal is likely to be high.

Table 2: Factors informing the coping appraisal construct.

| Perceived Factor | High Level | Coping Appraisal Level |

| Perceived Self-Efficacy | Yes | High |

| Perceived Response Efficacy | Yes | |

| Perceived Cost (Adaptive Response) | No |

People who believe they have the skills, resources and knowledge required to cope effectively with a bushfire are likely to have a high coping appraisal. This can be achieved by investing in fireproof materials, having access to reliable sources of information and support and having experience responding to previous bushfires (Mortreux, O’Neill & Barnett 2020). However, if a person perceives high costs associated with responding to a bushfire, such as leaving their home and possessions behind, their coping appraisal is likely low. Those with financial resources to invest in fireproof materials and evacuation plans may perceive low-cost levels and have a high coping appraisal Wilson et al. (2020).

Self-evacuation decision-making matrix

Self-evacuation is a critical decision people make during a bushfire. Several factors, including threat and coping appraisal, influence the self-evacuation decision. Threat appraisal refers to the perception of danger or risk associated with an event while coping appraisal refers to an individual’s perceived ability to cope with and manage the consequences of the event via self-evacuation. The decision matrix (Table 3) incorporated in the framework (Figure 9) uses these 2 factors to categorise householders into 4 different scenarios, each with its own recommended self-evacuation decision.

Table 3: Self-evacuation decision-making matrix.

| Threat Appraisal | |||

| High | Low | ||

| Coping Appraisal | High | Tendency to evacuate | Less likely to evacuate |

| Low | Less likely to evacuate | Tendency to not evacuate | |

High threat appraisal and high coping appraisal

Householders who perceive a high level of danger, threat and the timing of impact and believe they have necessary resources and abilities to cope with the situation, are more likely to evacuate. According to Losee, Webster and McCarty (2022) and Stancu et al. (2020), individuals who perceive a high level of danger and have high coping resources are more likely to evacuate because they believe they can accommodate the consequences of the disaster. If a householder perceives a high threat and can cope with the situation, they are likely to evacuate. Therefore, increased threat and coping appraisal equals increased likelihood of evacuation.

High threat appraisal and low coping appraisal

Householders who perceive a high level of danger but have limited coping resources are less likely to evacuate. In these situations, the high threat appraisal is unlikely to override any concerns about evacuation costs (Ntzeremes, Kirytopoulos & Filiou 2020, Simpson et al. 2021). If a person perceives a high threat but cannot cope with the situation, they are less likely to evacuate despite the high perceived threat. Therefore, increased threat and decreased coping appraisal equals decrease likelihood of evacuation.

Low threat appraisal and high coping appraisal

Householders who perceive a low level of danger and have high coping resources are less likely to evacuate. These people may believe they can manage the consequences of the event and are not motivated to evacuate (Fraser, Morikawa & Aldrich 2021, Shoji & Murata 2021). If a person perceives a low threat but has a high ability to cope with the situation, they are less likely to evacuate because their coping appraisal is high. Therefore, decreased threat and increased coping appraisal equals decreased likelihood of evacuation.

Low threat appraisal and low coping appraisal

Householders who perceive a low level of danger and have limited coping resources are not likely to evacuate. These people may not perceive the need to evacuate, given their low threat appraisal and limited coping resources (Berlin Rubin & Wong-Parodi 2022, Katzilieris, Vlahogianni & Wang 2022). If a person perceives a low threat and cannot cope with the situation, they are unlikely to evacuate. Therefore, decreased threat and coping appraisal equals decreased likelihood of evacuation.

Role of incentives in bushfire crisis management

Table 4 Shows how the concept of incentives could fit within the construct of prevention, mitigation, preparedness, response and recovery. By incorporating incentives into each phase of bushfire management, governments and communities can encourage proactive actions, promote resilience and support the recovery process.

Table 4: Fitting Incentives into the phases of bushfire crisis management.

| S/N | Phase | How incentives could fit in the phases |

| 1 | Prevention | Incentives can encourage individuals and communities to undertake activities that prevent bushfires. For example, governments can offer financial incentives or grants to homeowners who take measures to reduce fire hazards around their properties, such as clearing vegetation or installing fire-resistant roofing. Incentives can also be provided for communities that develop and implement effective fire-prevention plans. |

| 2 | Mitigation | Incentives can bolster endeavours that lessening the repercussions of bushfires. This could entail compensating landowners or farmers who reduce fuel loads, such as controlled burns or strategic grazing. In addition, incentives can be extended to businesses and industries that adopt fire-resistant building materials and firebreaks to safeguard infrastructure. |

| 3 | Preparedness | Incentives to individuals and households who create and maintain comprehensive bushfire survival plan that includes evacuation routes and communication planning can be a great motivator. For example, discounted insurance premiums. Additionally, incentives could motivate communities to establish volunteer firefighting units and participate in training programs to enhance their levels of preparedness. |

| 4 | Response | Incentives that inspire individuals to take active parts in responding to bushfires. These may include financial or tangible benefits for volunteers in firefighting or emergency services. Incentives might also be extended to businesses that provide resources or services during the response phase, such as offering equipment or shelter for people who have been displaced, both human and animals. |

| 5 | Recovery | Incentives in the recovery phase might involve financial grants to businesses and individuals for rebuilding homes, infrastructure and local economies. Additionally, incentives can be offered to attract tourists and investors to the affected areas (when appropriate) to aide in the financial recovery of tourism and other business. |

Implications and conclusion

The findings from this study suggests that financial and non-financial incentives like insurance, government programs, clear warning systems and evacuation legislation can motivate householders to self-evacuate from bushfire-prone areas. Such incentives align with the Protection Motivation Theory, which posits that individuals are more likely to engage in protective behaviour when they perceive a level of threat and have the necessary resources and motivation to act. However, the effectiveness of incentives may vary depending on specific contexts and appreciation of threats among various householders. Therefore, policymakers and emergency management agencies can benefit from these findings to design appropriate incentives that could encourage people to self-evacuate from bushfire-prone areas.

Early self-evacuation saves lives. Appreciation of threat and coping appraisals could influence the decision to evacuate. For example, high danger perception and coping resources increase the likelihood of evacuation, while low danger perception and limited coping resources decrease it. The framework encompasses input, process and output components. First, the input component involves incentives that motivate people to prioritise their safety during bushfires, including information and communication, adequate resourcing of the fire services, emergency accommodation, bushfire education programs, vegetation management, financial assistance, access roads, security and property protection, affordable insurance coverage, alternative power supplies, property preparation assistance, return access to properties and improved development approval procedures. Collectively these can reduce self-evacuation costs and increase the perceived benefits of protective behaviour. Second, the process component focuses on the cognitive assessment phase of people when faced with the decision to self-evacuate, guided by the Protection Motivation Theory. Third, the output component encompasses the resulting evacuation decisions made by householders: the tendency to evacuate, less likely to evacuate and tendency not to evacuate indicated in self-evacuation decisions framework. These decisions can be tailored to individual needs to enhance community resilience and promote self-evacuation in bushfire emergencies.