Towards effective mitigation strategies for severe wind events

Daniel J Smith, Connor McShane, Anne Swinbourne, David J Henderson

Peer-reviewed Article

Abstract

Article

Introduction

Australia’s annual insured losses due to natural disasters exceed $480 million on average (Insurance Council of Australia 2014), highlighting the need for stronger homes and infrastructure. In Queensland, there were eight natural disasters between November 2014 and May 2015 resulting in government funding assistance activations (Queensland Government 2015). Increasing population densities in Queensland coastal regions also increase exposure of built environments, particularly to severe wind events (Middelmann 2007). For example, Cyclone Yasi in 2011 required $800 million to rebuild assets and provide community support (Queensland Government 2011), despite making landfall outside of major northern Queensland cities.

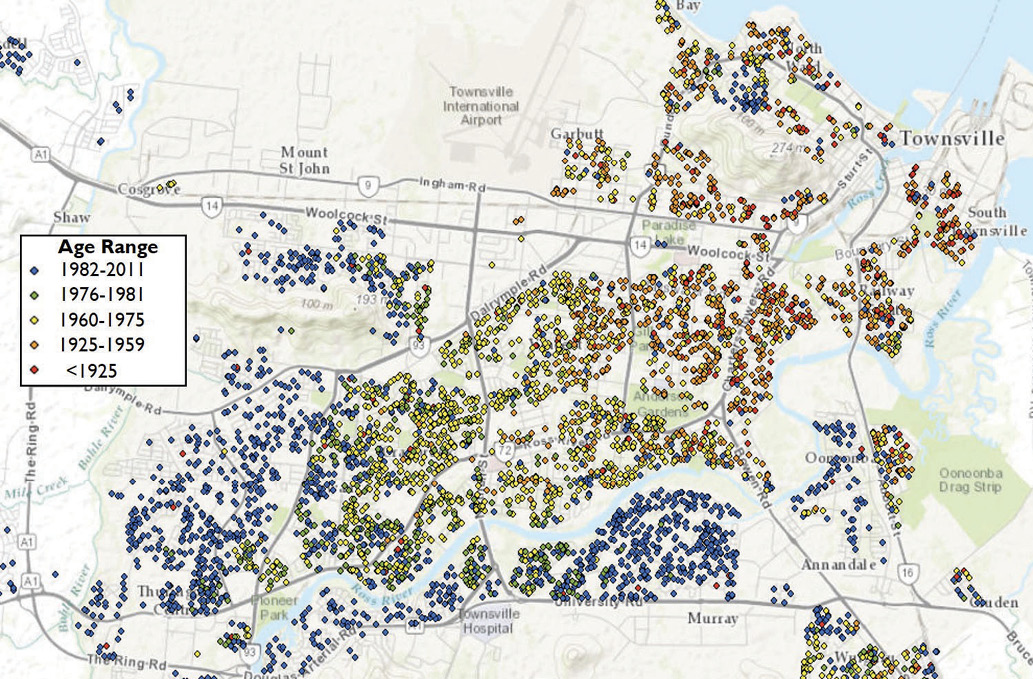

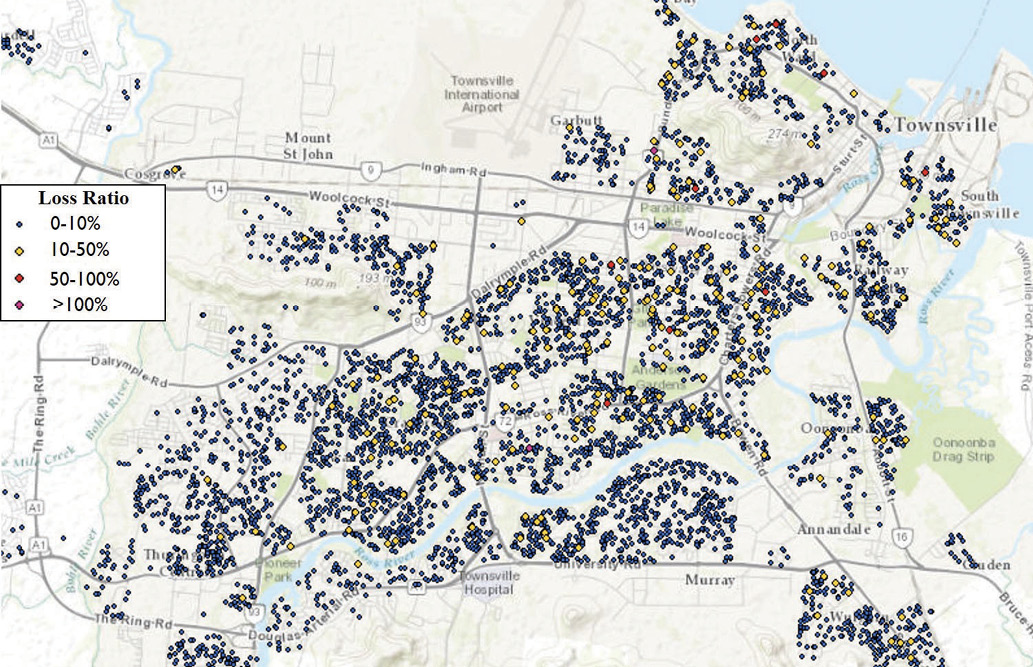

A preliminary analysis of claims data (Figure 1 and Figure 2) from Cyclone Yasi (Smith & Henderson 2015a) shows that both legacy and contemporary housing have vulnerabilities that modulate the extent of loss during a cyclone. Building science research consistently shows that losses induced by severe wind events can be minimised if appropriate mitigation activities are employed (Grayson & Pang 2014, Pinelli et al. 2009, Smith & Henderson 2015b, Smith, Henderson & Ginger 2015).

Figure 1: Distribution of construction ages for housing in Townsville, Australia for policies from one insurer (Smith & Henderson 2015a).

Figure 2: Distribution of loss ratio (i.e. claim value divided by sum insured value) for policies in Townsville, Australia from one insurer for Cyclone Yasi in 2011 (Smith & Henderson 2015a).

From an engineering perspective, appropriate methods of cyclone loss mitigation have been discussed extensively in the literature. These vary by construction type, age, location, etc. but generally include:

- increasing the wind uplift resistance of the house structure (Lavelle & Vickery 2013, Leatherman, Chowdhury & Robertson 2007)

- sealing the building envelope from water ingress (Lopez, Masters & Bolton 2011)

- securing items outside the house that are susceptible to wind uplift (e.g. outdoor furniture, yard equipment, etc.).

However, post-event damage assessments conducted over the last 15 years by the Cyclone Testing Station (www.cyclonetestingstation.com) show that engineering solutions to wind vulnerability, particularly for older homes, are not being widely implemented (Boughton & Falck 2007, Boughton et al. 2011, Henderson et al. 2006). This is due in large part to the absence of community engagement activities with respect to engineering solutions for risk mitigation. For example, the ‘Get Ready Queensland’ program is an important community outreach program that emphasises general disaster preparedness education (i.e. trimming trees, emergency kits, and evacuation plans) but does not identify engineering deficiencies and facilitate associated solutions, which typically drive severe losses during cyclones.

Engineering solutions to help buildings, particularly older buildings, cope during high winds are not widely implemented. Image: Cyclone Testing Station, James Cook University.

To provide experiential insight, examples of mitigation incentives implemented in the south-east USA since 2005 have been reviewed and are discussed. Despite measureable success in some of these approaches, wind vulnerability is still a major issue for the region. It is contested that higher levels of effectiveness can be achieved by developing engineering and community engagement solutions in parallel. Focusing here on the latter, typical drivers of mitigation behaviour (by homeowners) from the literature are presented. Finally, a smartphone application is discussed as a potential mitigation tool to stimulate mitigation actions in Australia and the USA.

Existing approaches

Existing mitigation approaches include the responses to average insured tropical cyclone losses from 2003 to 2012 ranging US$3-30 billion annually (Property Claim Services 2014). Florida is at the forefront, largely due to experience. Category 1-3 hurricane landfalls in Florida are biennial and Category 4-5 landfalls are quadrennial on average (Malmstadt, Scheitlin & Elsner 2009). Government and private funding schemes, premium reductions, and vulnerability rating systems are included.

Property Assessed Clean Energy (PACE) funding program

The PACE funding program in the USA is delivered by private companies and offers long-term loans to strengthen and retrofit homes (Florida PACE Funding Agency 2015). The program was originally developed in California for earthquake mitigation and now operates in conjunction with local governments in Florida to provide loans for eligible residents to undertake risk-reducing home improvements (e.g. window protection for debris impact). Works are done through state-approved contractors. The loans are available for commercial and residential buildings as long as they are covered by existing insurance. The government also provides financial security for mortgage lenders to reduce financial risks associated with defaults on mortgages. The length of the loan, which has repayment priority over a mortgage, is approximately 15-20 years and is attached to the building as opposed to the owner. These conditions have generated a degree of concern about the financial risk involved for an individual undertaking the loan (Federal Housing Finance Agency 2010).

Past evaluations in other states in the USA have reported success in acceptance of the program by residents as well as considerable economic benefits for the immediate community and broader population (Saha 2012). For example, in Boulder County, Colorado, a PACE program funded US$9.8 million in residential retrofit projects in the first phase of delivery (Goldberg, Clinburn & Coughlin 2011). The program also contributed an estimated US$14 million in economic activity for the county. Therefore, despite potential financial concerns, programs like PACE can be beneficial for regional communities by reducing structural vulnerability and enhancing the economic well-being of the region.

Cyclone Marcia caused significant damage to property in Yeppoon, Queensland due to its severe winds and the way properties were constructed. Image: Cyclone Testing Station, James Cook University.

‘My Safe Florida Home’ program

The ‘My Safe Florida Home’ program is administered in Florida by the Department of Financial Services and was operated from 2007 to 2009 (the 2008 economic crisis pre-empted additional funding). This US$250 million program offered homeowners free assessment of their home for structural vulnerabilities and allowed them to apply for a US$5000 grant to retrofit their homes. Assessment findings were provided to the homeowner in a report that outlined appropriate structural improvements, the cost, and the associated insurance discount if improvements were completed. The program targeted lower-socio-economic owners of older single-family homes in high-wind risk regions. This provided an equitable approach to strengthening homes for those who would otherwise have been unable to afford it. The program delivered 401,372 home inspections and included over US$80 million in mitigation grant reimbursements (Chapman-Henderson & Rierson 2015). An estimated 55 per cent of inspected homes were eligible for an average US$217 premium discount, with potential state-wide insurance savings of US$24.5 million (Sink 2008), assuming retrofits were carried out.

A 2009 evaluation by Risk Management Solutions estimated that ‘My Safe Florida Home’ ‘reduced the 100-year probable maximum loss (PML) by at least US$1.50 per dollar invested in grants’ and that the reduction was equivalent to a reduction of approximately US$140 million in the 100-year PML of US$61.9 billion (Young 2009). A study by Chatterjee and Mozumder (2014) also found that residents who had home insurance, prior experience with damages, and a heightened sense of vulnerability were more likely to seek home inspection as part of the program. Other hurricane-prone USA states including Alabama, Louisiana, Mississippi, and South Carolina adopted and implemented similar initiatives.

FORTIFIED Program

The FORTIFIED program, developed by the Insurance Institute for Business and Home Safety (IBHS) in the USA, provides gold, silver and bronze resilience standards for homes with corresponding guidelines for both homeowners and insurance companies (IBHS 2013). The standards provide detailed construction requirements for each rating level, including guidelines for retrofitting. Laws and regulations are adopted at the state-level for providing insurance and other financial incentives based on the level of standard adopted. For example, in 2013 the Georgia Underwriting Association adopted a mitigation strategy that recognises the program by providing credits for the wind-risk component of insurance under the homeowners and dwelling programs. The credits include 5 per cent for Bronze, 7.5 per cent for Silver, and 10 per cent for Gold. A similar policy in Mississippi offers 17 per cent for Bronze, 25 per cent for Silver, and 30 per cent for Gold (IBHS 2013). The FORTIFIED program standards have been adopted in Alabama, Georgia, Mississippi and North Carolina.

These programs focus on perceived financial benefit (Poussin, Botzen & Aerts 2014); an obvious driver of preparedness action. Although financial incentives are an important motivator (Boon 2013), they do not ensure mitigation action. A public opinion survey during the ‘My Safe Florida Home’ program found that only 40 per cent of respondents indicated that reduced insurance premiums were a key motivator in undertaking improvements to their home (Sink 2008). Financial incentives of this nature are more likely to be effective if used in concert with other behavioural drivers.

Severe roofing failure due to weak roof framing connections in properties happened during Cyclone Marcia in 2015 in Yeppoon, Queensland. Image: Cyclone Testing Station, James Cook University.

Behavioural drivers

Missing from the existing approaches is a holistic perspective on what drives individuals to take mitigation actions. Each of the programs reviewed hinge on financial incentive and fail to encompass other motivators. Identifying other incentives can be difficult as they can be situationally and contextually specific to the individual. Factors affecting the success of mitigation activities therefore differ by region, event type, and citizen-behaviour patterns. Four key factors were identified in the literature that show factors beyond financial incentive.

Prior event experience

The prior experience an individual has with weather events can have both positive and negative effects on their likelihood of engaging in preparedness action. Research demonstrates that those who have a negative prior experience with disaster or extreme weather events are more likely to prepare for future events (Boon et al. 2012, Paton, Smith & Violanti 2000). However, those experiencing minimal damage or loss during prior events may have biased perceptions of risk resulting in an underestimation of event consequences or overestimation of the effectiveness of preparatory actions. The findings of a 2013 Queensland homeowner survey supports this concept (Inspector-General Emergency Management 2014). A perception study exposed participants to varying wind fields and asked them to estimate the speed and corresponding risk they felt (i.e. higher perceived wind speed, greater perceived risk). Agdas and colleagues (2012) found that individuals with prior experience of cyclones were more accurate in their estimations and, therefore, more accurately understood the risk.

Mitigation capacity

Mitigation capacity refers to an individual’s:

- knowledge of risks associated with the hazard

- knowledge of actions to reduce risk

- ability to execute those actions.

For example, Mishra and Suar (2012) show that individuals who have greater preparedness education and access to resources (e.g. income, education, social resources) are more likely to adequately prepare. Thus, it is important to identify barriers and enablers of education and resources for mitigation within the target community or region.

Social connectedness

Social connectedness includes the shared experience, reciprocity and trust individuals have toward one another within a community (Cocklin & Alston 2002, Malecki 2011). For example, homeowner cost-benefit evaluation of an action can be influenced by who is recommending the action (Pennings & Grossman 2008, Ramirez, Antrobus & Williamson 2013). In a survey of Florida homeowners, 40 per cent of respondents reported being more likely to undertake improvements to their home if others in the community were also strengthening their homes (Sink 2008). This is consistent with findings from Ramirez and colleagues (2013), that suggests people are more likely to respond in a manner similar to those with whom they have connections and trust (i.e. neighbours and friends) than unfamiliar entities (e.g. hypothetical exemplars in promotional materials). Therefore, understanding and leveraging the nature of relationships individuals have within communities can increase the effectiveness of strategy implementation.

Understanding and leveraging the nature of relationships individuals have within communities can increase the effectiveness of strategy implementation.

Freedom of choice

Freedom of choice is a critical and often understated component of a homeowner’s decision-making process for undertaking mitigation actions. The ability to choose how, when, and why to participate, offers a sense of ownership in the action plan. This helps to promote positive feelings (e.g. sense of accomplishment) about the experience, which increases the likelihood of taking additional actions and communicating the experience to peers. Control over choice is consistently associated with increased probability of performing an action (Brody, Glover & Vedlitz 2011, Sattler, Kaiser& Hittner 2000). This is further supported by Sink (2008), which indicates that survey respondents valued something they could choose to do rather than actions forced upon them.

Resilient Residence

ResilientResidence, or ‘ResRe’, is a prototype smartphone tool that is being developed in parallel in Florida and Queensland through a partnership between engineering and behavioural science researchers at the University of Florida (Prevatt & Florig 2015) and James Cook University (Smith et al. 2015). The application provides a specific wind-risk assessment of the user’s home, including an estimate of anticipated losses that would occur in a scenario event (e.g. Category 2 cyclone). In addition, based on data supplied by the user, the tool suggests appropriate retrofit solutions. Without a complete mental picture of the key behavioural drivers, it is difficult to determine the right parcel of incentives. Therefore, development focus of ResRe is on understanding the mental models (e.g. decision trees) that homeowners have when it comes to mitigation actions for hazards.

Screen captures of current wire-frame U.S. version of ResilientResidence™ including building attribute selection (left) and attribute help screens (right).

Discussion

In developing new ways for Australians to identify and assess risk and take meaningful mitigation actions, the experience of previous efforts from the USA should be leveraged. Vulnerability rating systems (e.g. FORTIFIED) can be a valuable tool to facilitate the interaction between engineering-based risk assessment and risk-reflective pricing in the insurance industry, providing financial incentive for retrofitting. The required framework for the system is already in place. Some insurers in Queensland now offer premium reductions for household upgrades in cyclone-prone regions. Reductions should be used in tandem with loan assistance (e.g. PACE) or government-supported grant programs (e.g. ‘My Safe Florida Home’) to help realise the more costly upgrades that otherwise would not be financially viable. Such programs can stimulate growth in construction and manufacturing industries as new, more cost effective retrofit products are developed. In the longer term, risk-reflective pricing in real estate markets can also be used to support mitigation.

Ultimately, the onus to protect a home falls on those living in it. There are a range of mitigation support efforts that can and should be used to support that decision-making process. However, those efforts must incorporate a holistic understanding of an individual’s decision process to turn increased understanding and knowledge about risk exposure into mitigation actions to increase household, and thus, community resilience.

| Acknowledgements

This research was supported by a Queensland Government Advance Queensland Research Fellowship and the Bushfire and Natural Hazards Cooperative Research Centre. The authors acknowledge the valued contributions from Suncorp and Dr David Prevatt and David Roueche of the University of Florida. Any opinions, findings, conclusions, or recommendations expressed in this article are those of the authors and do not necessarily reflect the views of the sponsors, partners, or contributors. |

References

Agdas D, Webster GD & Masters FJ 2012, Wind Speed Perception and Risk. Plos One 7, e49944.

Boon H, Cottrell A, King D, Stevenson R & Millar J 2012, Bronfenbrenner’s bioecological theory for modelling community resilience to natural disasters. Natural Hazards vol. 60, pp. 381-408.

Boughton G & Falck D 2007, Tropical Cyclone George damage to buildings in the Port Hedland area. Cyclone Testing Station, James Cook University, Townsville. TR 52.

Boughton GN, Henderson DJ, Ginger JD, Holmes JD, Walker GR, Leitch C, Somerville LR, Frye U, Jayasinghe NC & Kim P 2011, Tropical Cyclone Yasi structural damage to buildings. Cyclone Testing Station, James Cook University, Townsville. TR 57.

Brody S, Grover H & Vedlitz A 2011, Examining the willingness of Americans to alter behaviour to mitigate climate change. Climate Policy 12, pp. 1-22.

Chapman-Henderson L & Rierson AK 2015, Understanding the intersection of resilience, big data, and the internet of things in the changing insurance marketplace, 14th Biennial Aon Benfield Hazards Conference, September 21-23, Gold Coast, Australia.

Chatterjee C & Mozumder P 2014, Understanding household preferences for hurrican risk mitigation information: Evidence from survey responses. Risk Analysis vol. 34, pp. 984-996.

Cocklin C & Alston M 2002, Community sustainability in rural Australia: A question of capital? Academy of the Social Sciences in Australia, Wagga Wagga, NSW.

Federal Housing Finance Agency 2010, Statement on Certain Energy Retrofit Loan Programs.

Florida PACE Funding Agency 2015, Florida PACE Funding Agency.

Goldberg M, Cliburn JK & Coughlin J 2011, Economic impacts from the Boulder County, Colorado, ClimateSmart Loan Program: Using Property-Assessed Clean Energy (PACE) Financing. National Renewable Energy Laboratory.

Grayson J & Pang W 2014, The Influence of Community-Wide Hurricane Wind Hazard Mitigation Retrofits on Community Resilience, Structures Congress 2014. American Society of Civil Engineers, pp. 1392-1402.

Henderson D, Ginger J, Leitch C, Boughton G. & Falck D 2006, Tropical Cyclone Larry damage to buildings in the Innisfail area. Cyclone Testing Station, James Cook University, Townsville, QLD.

Inspector-General Emergency Management 2014, Queensland Community Preparedness Survey November 2013.

Institute for Business and Home Safety (IBHS) 2013, Insurer’s guide to FORTIFIED.

Insurance Council of Australia 2014, Historical Disaster Statistics. Insurance Council Australia. At: www.insurancecouncil.com.au/industry-statistics-data/disaster-statistics/historical-disaster-statistic [11 September 2014].

Lavelle FM & Vickery PJ 2013, Interactions among Wind Mitigation Features in Benefit/Cost Analysis, Advances in Hurricane Engineering, pp. 1067-1077.

Leatherman SP, Chowdhury AG & Robertson CJ 2007, Wall of Wind Full-Scale Destructive Testing of Coastal Houses and Hurricane Damage Mitigation. Journal of Coastal Research, pp. 1211-1217.

Lopez C, Masters FJ & Bolton S 2011, Water penetration resistance of residential window and wall systems subjected to steady and unsteady wind loading. Building and Environment 46, pp. 1329-1342.

Malecki EJ 2011, Regional Social Capital: Why it Matters. Regional Studies 46, pp. 1023-1039.

Malmstadt J, Scheitlin K & Elsner J 2009, Florida Hurricanes and Damage Costs. Southeastern Geographer 49, pp. 108-131.

Middelmann MH 2007, Natural hazards in Australia: Identifying risk analysis requirements, in: Department of Industry, T.R. (Ed.). Geoscience Australia, Canberra.

Mishra S & Suar D 2012, Effects of Anxiety, Disaster Education, and Resources on Disaster Preparedness Behavior. Journal of Applied Social Psychology vol. 42, pp. 1069-1087.

Paton D, Smith L & Violanti J 2000, Disaster response: risk, vulnerability and resilience. Disaster Prevention and Management vol. 9, pp. 173-180.

PCS 2014, Inflation-Adjusted U.S. Insured Catastrophe Losses by Cause of Loss, 1994-2013. At: www.iii.org/fact-statistic/catastrophes-us [3 May 2015].

Pennings JME & Grossman DB 2008, Responding to crises and disasters: the role of risk attitudes and risk perceptions. Disasters vol. 32, pp. 434-448.

Pinelli JP, Torkian BB. Gurley K, Subramanian C & Hamid S 2009, Cost effectiveness of hurricane mitigation measures for residential buildings, in: Proceedings of the 11th Americas Conference on Wind Engineering.

Poussin JK, Wouter Botzen WJ & Aerts JCJH 2014, Factors of influence on flood damage mitigation behaviour by households. Environmental Science and Policy vol. 40, pp. 69-77.

Prevatt DO & Florig K 2015, Effectiveness of a smartphone-based decision support system to stimulate hurricane damage mitigation actions among homeowners in Coastal Hillsborough County, FL communities. Florida Sea Grant University of Florida, Gainesville, Florida.

Queensland Government 2011, Yasi damage bill set to top $800 million. The Queensland Cabinet and Ministerial Directory.

Queensland Government 2015, Disaster Relief Activations, in: Disaster Management (Ed.), Get Ready Queensland.

Ramirez S, Antrobus E & Williamson H 2013, Living in Queensland: Preparing for and communicating in disasters and emergencies. Australian Journal of Communication vol. 40.

Saha D 2012, Enact legislation supporting residential Property Assessed Clean Energy financing (PACE). in: Brookings Metropolitan Policy Program (Ed.), Strengthen Federalism, Renewing the Economy. Brookings.

Sattler DN, Kaiser CF & Hittner JB 2000, Disaster preparedness: Relationships among prior experience, personal characteristics, and distress. Journal of Applied Social Psychology vol. 30, pp. 1396-1420.

Sink A 2008, My Safe Florida Home Program, in: Proceedings of the Hurrican Risk Mitigation Forum.

Smith DJ & Henderson DJ 2015a, Insurance claims data analysis for Cyclones Yasi and Larry. CTS Technical Report TS1004.2.

Smith DJ & Henderson DJ 2015b, Cyclone Resilience Research – Phase 2. CTS Technical Report TS1018.

Smith DJ, Henderson DJ & Ginger JD 2015, Improving the wind resistance of Australian legacy housing, in: Proceedings of the 17th Australasian Wind Engineering Society Workshop.

Smith DJ, Roueche DB, Thompson AP & Prevatt DO 2015, A vulnerability assessment tool for residential structures and extreme wind events, in: Dilum Fernando, J.-G.T., Jose L. Torero (Ed.), Proceedings of the Second International Conference on Performance-based and Life-cycle Structural Engineering. School of Civil Engineering, The University of Queensland, Brisbane, Australia, pp. 1164-1171.

Young M 2009, Analyzing the Effects of the My Safe Florida Home Program on Florida Insurance Risk. Risk Management Solutions (RMS). At: www.sbafla.com/method/portals/methodology/AdditionalMaterialWMC/RMS_MSFH_Report_May_2009.pdf.

About the authors

Dr Daniel Smith is a research fellow with the Cyclone Testing Station. His research experience covers a wide range of wind engineering disciplines including structural retrofitting for wind and water ingress, vulnerability and fragility modelling, and behavioural aspects of community cyclone preparedness.

Dr Connar McShane is a lecturer in the discipline of Psychology. She has a strong research interest in how people perceive and respond to threats, particularly in rural and regional areas.

Dr Anne Swinbourne is a psychologist with experience in population level health promotion and disaster management interventions. The focus of her research is the investigation of the mechanisms by which community capacity to deal with weather events can be improved.

Dr David Henderson is Director of the Cyclone Testing Station investigating effects of wind loads on low rise buildings. He has broken everything from roofing screws through to complete houses, and led damage investigations following cyclones, thunderstorms and tornadoes.